All Categories

Featured

Table of Contents

If you pick level term life insurance, you can allocate your premiums due to the fact that they'll stay the same throughout your term. And also, you'll understand precisely how much of a survivor benefit your recipients will obtain if you die, as this amount will not transform either. The prices for level term life insurance policy will certainly rely on numerous variables, like your age, health and wellness status, and the insurance provider you select.

Once you go with the application and medical examination, the life insurance policy company will certainly review your application. They need to inform you of whether you've been approved shortly after you use. Upon approval, you can pay your initial premium and sign any type of pertinent documentation to ensure you're covered. From there, you'll pay your costs on a monthly or annual basis.

Aflac's term life insurance policy is practical. You can select a 10, 20, or 30 year term and appreciate the added assurance you are entitled to. Dealing with a representative can help you find a plan that functions ideal for your needs. Find out more and obtain a quote today!.

As you look for means to protect your economic future, you've likely found a large selection of life insurance policy choices. level term life insurance. Selecting the ideal coverage is a huge choice. You desire to discover something that will certainly help sustain your enjoyed ones or the reasons vital to you if something takes place to you

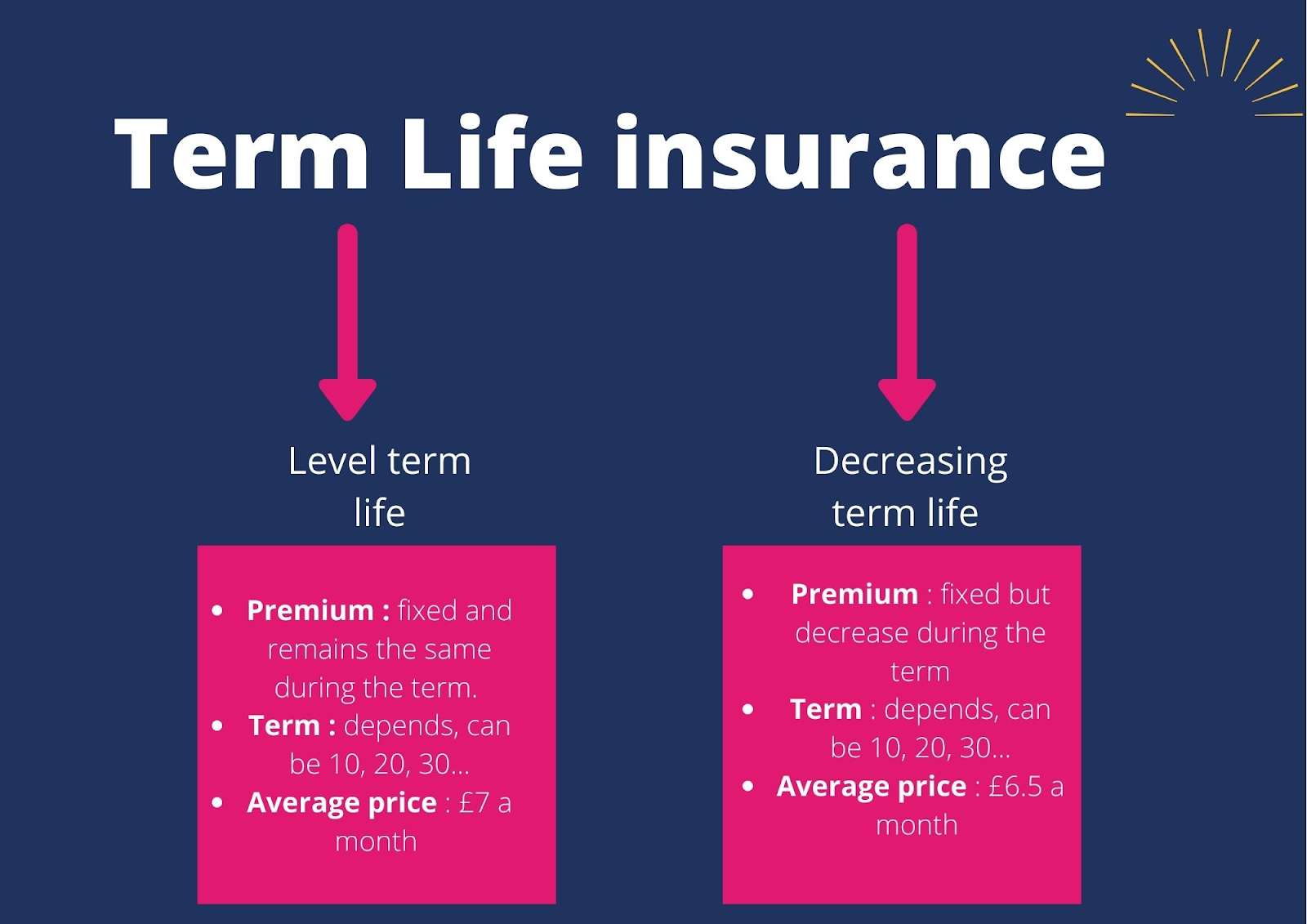

Lots of people favor term life insurance policy for its simpleness and cost-effectiveness. Term insurance agreements are for a fairly brief, specified time period but have alternatives you can customize to your requirements. Certain benefit options can make your premiums change with time. Degree term insurance coverage, nevertheless, is a kind of term life insurance policy that has constant repayments and a constant.

Cost-Effective Increasing Term Life Insurance

Degree term life insurance coverage is a subset of It's called "degree" due to the fact that your premiums and the advantage to be paid to your loved ones continue to be the exact same throughout the agreement. You will not see any modifications in expense or be left questioning its worth. Some contracts, such as every year sustainable term, might be structured with premiums that enhance in time as the insured ages.

They're determined at the beginning and continue to be the same. Having regular payments can aid you far better plan and budget plan due to the fact that they'll never change. Dealt with death benefit. This is also evaluated the start, so you can recognize precisely what fatality benefit amount your can anticipate when you die, as long as you're covered and current on costs.

You concur to a set costs and death benefit for the duration of the term. If you pass away while covered, your fatality advantage will certainly be paid out to loved ones (as long as your costs are up to day).

You might have the choice to for an additional term or, more likely, restore it year to year. If your contract has actually an ensured renewability provision, you may not need to have a new medical test to keep your coverage going. Your costs are most likely to boost because they'll be based on your age at renewal time.

With this alternative, you can that will certainly last the rest of your life. In this situation, once again, you may not need to have any new medical tests, however premiums likely will rise as a result of your age and new protection. which of these is not an advantage of term life insurance. Different firms use different alternatives for conversion, be sure to recognize your choices prior to taking this action

Value Which Of These Is Not An Advantage Of Term Life Insurance

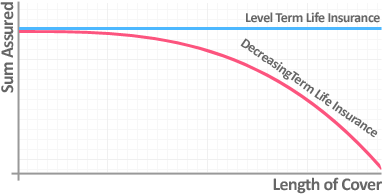

Consulting with a financial expert additionally might help you identify the course that straightens finest with your overall strategy. The majority of term life insurance policy is level term throughout of the agreement period, but not all. Some term insurance might come with a premium that enhances gradually. With lowering term life insurance policy, your fatality benefit goes down in time (this kind is often secured to particularly cover a long-term financial obligation you're paying off).

And if you're set up for sustainable term life, then your costs likely will rise every year. If you're exploring term life insurance policy and want to guarantee simple and foreseeable financial defense for your household, degree term may be something to think about. However, as with any kind of kind of coverage, it may have some limitations that do not fulfill your needs.

Level Term Life Insurance Meaning

Commonly, term life insurance policy is more inexpensive than permanent insurance coverage, so it's a cost-effective means to protect economic defense. Adaptability. At the end of your contract's term, you have several choices to continue or move on from coverage, commonly without needing a medical exam. If your spending plan or insurance coverage needs change, survivor benefit can be decreased over time and cause a lower premium.

As with other kinds of term life insurance policy, when the contract ends, you'll likely pay higher costs for protection due to the fact that it will certainly recalculate at your existing age and health and wellness. If your monetary circumstance changes, you might not have the necessary protection and could have to purchase extra insurance.

That does not mean it's a fit for everyone. As you're shopping for life insurance policy, below are a few key elements to think about: Budget. One of the advantages of degree term insurance coverage is you recognize the expense and the death benefit upfront, making it much easier to without stressing over rises gradually.

Age and wellness. Normally, with life insurance coverage, the healthier and more youthful you are, the a lot more cost effective the coverage. If you're young and healthy and balanced, it might be an attractive alternative to lock in reduced costs now. Financial duty. Your dependents and monetary obligation contribute in identifying your insurance coverage. If you have a young family members, as an example, level term can aid offer financial backing throughout important years without paying for coverage much longer than required.

1 All riders go through the terms of the cyclist. All bikers might not be offered in all territories. Some states might vary the terms and problems (term 100 life insurance). There may be an extra charge related to acquiring certain bikers. Some bikers may not be offered in mix with other motorcyclists and/or policy features.

2 A conversion credit report is not offered for TermOne policies. 3 See Term Conversions area of the Term Series 160 Product Guide for how the term conversion credit report is identified. A conversion credit scores is not offered if costs or charges for the brand-new policy will be forgoed under the terms of a rider supplying impairment waiver advantages.

Proven Group Term Life Insurance Tax

Policies transformed within the first policy year will certainly get a prorated conversion credit subject to conditions of the plan. 4 After five years, we reserve the right to restrict the permanent item provided. Term Series products are released by Equitable Financial Life Insurance Coverage Firm (Equitable Financial) (NY, NY) and are co-distributed by Equitable Network, LLC (Equitable Network Insurance Coverage Company of The Golden State, LLC in CA; Equitable Network Insurance Coverage Firm of Utah in UT; and Equitable Network of Puerto Rico, Inc. Term Life Insurance Policy is a sort of life insurance coverage plan that covers the insurance holder for a particular quantity of time, which is referred to as the term. The term lengths differ according to what the individual chooses. Terms usually range from 10 to three decades and rise in 5-year increments, providing degree term insurance policy.

{kind=link}

Latest Posts

Whole Life Final Expense Insurance

Funeral Funds For Seniors

Paying For Funeral With Life Insurance